If you’ve been exploring the world of philanthropy and charitable giving, you may have come across the term “Donor-Advised Fund.” But what exactly is a Donor-Advised Fund (DAF)?

A Donor-Advised Fund is a giving vehicle that allows individuals, families, or organizations to make charitable contributions, receive immediate tax deductions, and recommend grants to qualified nonprofit organizations.

When establishing a DAF, donors contribute cash, securities, or other eligible assets to a sponsoring organization.

Some organizations accept appreciated assets such as privately held stock, LLC business interests, and even privately held C corp shares, which gives the donor favorable tax advantages.

While donors maintain advisory privileges over the funds, the sponsoring organization assumes legal control.

This structure grants donors the flexibility to support multiple charitable causes over time, while the sponsoring organization handles administrative tasks and investment management.

DAFs provide a streamlined, tax-efficient, and strategic approach to charitable giving, enabling donors to make a lasting impact on causes they care about.

More importantly, it simplifies giving, allowing donors to handle their giving all from one place.

For example, if a donor gives to 10 charities over the course of 12 months, they typically need 10 receipts.

If they give to a DAF, they give one time, get one receipt, and can then recommend 10 grants to 10 qualified charities over time.

In this article*, we’ll dive deep into:

- • How Donor-Advised Funds work.

- • Their advantages and disadvantages.

- • How to set up a DAF.

- • Rules to keep in mind.

- • How they compare to other charitable giving vehicles.

So, let’s get started!

Learn more about Donor-Advised Funds by watching the video above!

Donor-Advised Funds Pros & Cons

DAFs have gained popularity as a flexible and efficient tool for charitable giving. Like any financial vehicle, DAFs have their advantages and disadvantages.

Let’s explore them to help you make an informed decision about whether a DAF is the right charitable giving option for you.

Advantages of Donor-Advised Funds

There are several benefits of Donor-Advised Funds for individuals and families who wish to make a meaningful impact through charitable giving.

Here are some key benefits.

Simplicity & Flexibility

Donor-Advised Funds provide a straightforward and flexible way to manage your charitable donations. You can make contributions to the fund and then recommend grants to your favorite charities over time.

This ensures all of your giving comes from one place, resulting in one receipt during tax season.

Immediate Tax Benefits

By contributing to a Donor-Advised Fund, you can receive an immediate tax deduction for the full value of your donation. Starting in 2026, for those who itemize, the deduction applies to your charitable gifts exceeding 0.5% of your adjusted gross income.

This allows you to potentially reduce or eliminate capital gains taxes that you would have incurred if you had sold the assets yourself. Once assets are contributed to a Donor-Advised Fund, they can grow tax-free.

Also, while the funds are held within the DAF, any investment growth or income generated by those assets grows tax free. This allows donors to maximize their charitable impact while minimizing their tax liability.

Utilization of Mutual Funds

When donors contribute to a DAF, they can choose from a selection of mutual funds or other investment choices that are offered by the fund provider.

These mutual funds provide diversification and professional management of the assets within the DAF, helping to potentially grow the funds over time.

Donors can select mutual funds based on their:

- • Risk tolerance.

- • Investment objectives or investment allocations.

- • Alignment with their philanthropic goals.

It’s important to note that not all DAFs offer this option. Some may charge an extra investment management fee for this service.

Long-Term Giving Strategy

Donor-Advised Funds enable you to take a strategic approach to philanthropy. You can contribute to the fund during high-income years and recommend grants to charities over time, even during a period of time when your financial situation might change.

Family Involvement

Donor-Advised Funds can involve multiple generations of a family in charitable giving. This can help instill philanthropic values in younger family members and create a lasting legacy of giving.

7 Ways To Give Smarter

Learn how to create a giving strategy that aligns your resources, values, and goals to make a meaningful difference.

Topics include:

— Donor-advised funds

— Donating stocks

— Donating from your IRA

— Optimizing your business sale

Download Our Guide to Smarter Giving!

Start your journey toward using your income to make a difference, leave a legacy, and enrich lives.

":" indicates required fields

Donor-Advised Funds Disadvantages

While Donor-Advised Funds offer many advantages, it’s essential to consider the potential drawbacks as well.

Here are a few disadvantages to be aware of.

Irrevocable Contributions

Once you contribute to a Donor-Advised Fund, the assets become the property of the fund sponsor. While you can recommend grants, you no longer have complete control over the donated assets.

Investment Management Fees

Donor-Advised Funds often charge administrative fees and investment management fees based on the assets in the fund. These fees can vary among different fund sponsors and may impact the overall amount available for charitable grants.

You should review these fees when considering a DAF as they will impact the growth of your funds.

Exclusion From Deduction for Standard Deduction Filers

Beginning in 2026, taxpayers taking the standard deduction may take an additional deduction for cash charitable donations (up to $1,000 for single filers or $2,000 for joint filers), but donations to donor-advised funds do not qualify.

How To Set Up a Donor-Advised Fund (8 Steps)

If you’re looking for a powerful and efficient way to manage your charitable giving, setting up a DAF might be the perfect solution.

Let’s walk through the step-by-step process of setting up a Donor-Advised Fund so you can begin your philanthropic journey with confidence.

Step 1: Research & Select a Fund Provider

The first step in setting up a Donor-Advised Fund is to research and select a reputable fund provider.

Consider factors such as:

- • The provider’s reputation.

- • Fees.

- • Investment options.

- • Customer service.

- • Any specific requirements they may have.

Step 2: Evaluate the Minimum Contribution Requirement

Each fund provider will have a minimum contribution requirement to establish a Donor-Advised Fund.

Evaluate the minimum contribution amount and ensure it aligns with your financial capacity.

The minimum requirement can vary between providers, so choose one that suits your needs.

Step 3: Initiate the Account Setup Process

Contact your chosen fund provider to initiate the account setup process.

They will guide you through the necessary instructions on how to make your initial contribution.

Step 4: Make an Initial Contribution

Once your account is set up, it’s time to make your initial contribution to the Donor-Advised Fund.

This can be in the form of:

- • Cash.

- • Appreciated securities.

- • Other eligible assets.

Consult with your fund provider to understand their specific guidelines and any restrictions on acceptable contributions.

Step 5: Receive Your Tax Deduction

One of the significant benefits of Donor-Advised Funds is the immediate tax deduction you can receive for your contributions.

Consult with your tax advisor to understand the tax implications and guidelines specific to your situation.

Obtain the necessary documentation from your fund provider to support your tax deduction claim, and ensure correct filing of your tax returns.

The deduction for appreciated assets that are donated to a DAF is limited to 30% of your adjusted gross income (AGI). (Amounts above this limit can be carried forward for up to five years.)

The deduction for donation of cash assets to a DAF is limited to 60% of your AGI. Appreciated assets such as real estate and privately held stock require a qualified appraisal to meet IRS guidelines.

Starting in 2026, for those who itemize, the deduction applies to your charitable gifts exceeding 0.5% of your adjusted gross income. (The 30% and 60% ceilings still apply.)

Step 6: Recommend Grant Distributions

With your Donor-Advised Fund established and funded, you can now start recommending grants to eligible charitable organizations.

Research and identify causes or nonprofits that align with your philanthropic goals. Most fund providers offer an online platform or a designated process to submit grant recommendations.

Provide the necessary details, such as:

- • The charitable beneficiary’s name.

- • Your address.

- • The purpose of the grant.

Step 7: Grant Review & Distribution

After you submit your grant recommendations, the fund provider will review them to ensure they comply with IRS regulations and the fund’s guidelines.

Once your recommendations are approved, the provider will distribute the grants to the designated charitable organizations on your behalf.

Some providers offer options for recurring grants or allow you to set a specific grant schedule.

Step 8: Monitor and Contribute Again to Your DAF

Once your Donor-Advised Fund is active, it’s essential to monitor and manage it regularly.

Stay informed about:

- • The fund’s performance.

- • Investment options.

- • Administrative processes.

Many providers offer online portals or tools to track your fund’s balance, grants, and contributions. Take advantage of these resources to ensure your fund aligns with your charitable goals over time.

Setting up a Donor-Advised Fund is a straightforward process that begins with selecting a reputable fund provider.

By following the step-by-step guide outlined above, you can:

- • Establish your Donor-Advised Fund.

- • Maximize your tax benefits.

- • Embark on a philanthropic journey that aligns with your values.

Remember to research your options, evaluate contribution requirements, and actively manage your fund to make a meaningful and lasting impact through charitable giving.

Donor-Advised Funds Rules (2025)

To make the most of your Donor-Advised Fund, it’s crucial to understand the rules associated with these charitable giving vehicles. While the specific rules may vary depending on the fund sponsor, here are some common guidelines:

Donor-Advised Funds vs. Private Foundations

When considering charitable giving options, it’s important to understand the differences between a Donor-Advised Fund and other common vehicles, such as private foundations and Charitable Remainder Trusts (CRTs).

Understanding these distinctions will help donors make informed decisions based on their philanthropic goals and preferences.

While both DAFs and private foundations allow you to support charitable causes, there are significant differences to consider:

DAF vs Private Foundation Aspects

| Aspect | Donor-Advised Fund | Private Foundation |

|---|---|---|

| Control | Donors retain advisory privileges over fund recommendations. | Donors have direct control over foundation’s activities. |

| Legal Entity | Not a separate legal entity; managed by a sponsoring organization. | Separate legal entity established by the donor. |

| Grant Recommendations | Donors recommend grants to qualified charities. | Trustees make grants to charitable causes. |

| Payout Requirements | No minimum payout required. | Required to distribute a certain percentage of assets annually. |

| Reporting Obligations | Donor involvement in grant recommendations. | Higher administrative and reporting responsibilities. |

| Startup Complexity | Generally simpler and faster to establish, often with no cost. | More complex legal and administrative requirements. Legal (and other) fees are often substantial. |

| Tax Deductions | Immediate tax deductions for contributions — up to 60% of adjusted gross income (AGI) for cash, 30% of AGI for assets like stock and real estate. (Note also the 0.5%-of-AGI floor for charitable deductions beginning in 2026.) | Immediate tax deductions for contributions, but lower deduction limits — 30% of AGI for cash contributions and 20% for assets like stock and real estate. (Note also the 0.5%-of-AGI floor for charitable deductions beginning in 2026.) |

| Overhead and Expenses | Managed by sponsoring organization; may have lower overhead. | Foundation bears administrative costs. |

| Valuation of Gifts | Fair market value. | The fair market value applies to publicly traded stock, while the cost basis is used for all other contributions, such as gifts of privately-held stock or real estate. |

| Excise Tax of Investment Income | None. | Typically an excise tax on 1.39% of net investment income annually. |

| Privacy | Individual donor names remain confidential and grants may be issued anonymously. | Must submit informational returns that are accessible to the public, revealing comprehensive details about grants, investment fees, trustee identities, staff salaries, and more. |

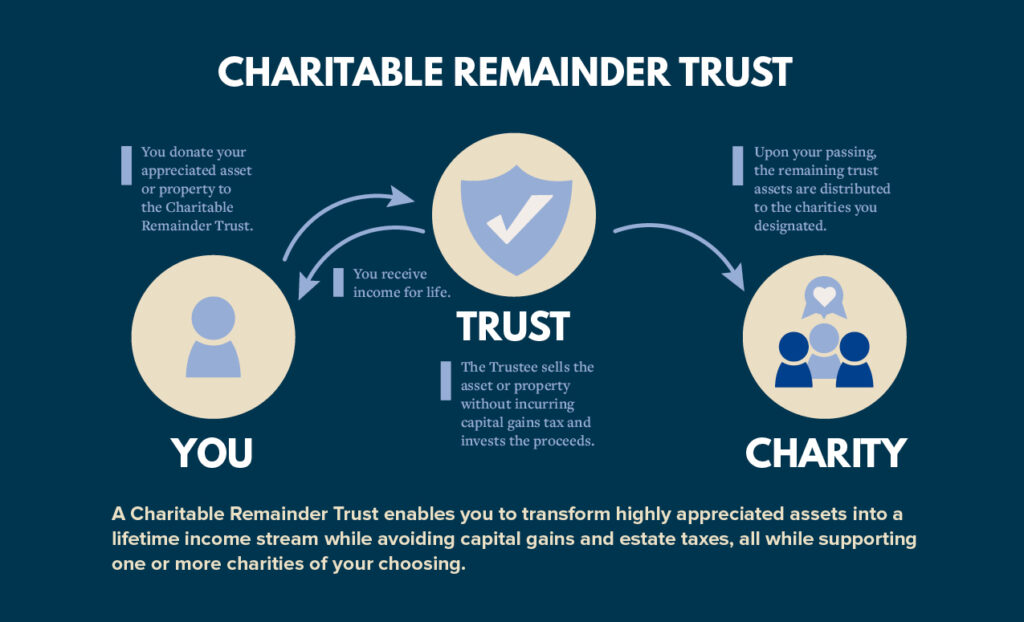

Donor-Advised Funds vs. Charitable Remainder Trust

Another charitable giving option often compared to Donor-Advised Funds is a Charitable Remainder Trust (CRT).

Here are some key distinctions between the two:

DAF vs Charitable Remainder Trust

| Aspect | Donor-Advised Fund | Charitable Remainder Trust |

|---|---|---|

| Setup | None, but there will likely be an annual administration fee. | Complex — legal and ongoing administration fees. |

| Timing of Gift | Donor makes an immediate contribution to the DAF and recommends grants to charities over time. | Donors receive income distributions for life and then the remainder goes to charity as the beneficiary. |

| Tax Deduction Limits for Cash Gifts | 60% of adjusted gross income (AGI). (Note also the 0.5%-of-AGI floor for charitable deductions beginning in 2026.) | Limited to the present value of the charitable organization’s remainder interest (value of the donated property minus the present value of the annuity). |

| Tax Deduction Limits for Gifts of Stock or Real Property | 30% of AGI. (Note also the 0.5%-of-AGI floor for charitable deductions beginning in 2026.) | Limited to the present value of the charitable organization’s remainder interest (value of the donated property minus the present value of the annuity). |

| Annual Minimum Distribution | No, grants are to charity. | Yes and distributions are taxable income to the donor. |

List of Donor-Advised Funds

When considering Donor-Advised Funds, it’s worth exploring a variety of options to find the one that aligns best with your philanthropic goals.

Here are some notable Donor-Advised Fund providers.

Best Donor-Advised Funds

Choosing the best Donor-Advised Fund for your philanthropic goals depends on various factors, including your preferences, investment options, fees, and support services.

Here are a few Donor-Advised Fund providers to consider:

Question: Can I Make an IRS QCD to Donor-Advised Fund?

No. A Qualified Charitable Distribution (QCD) is a powerful strategy that allows individuals age 70½ or older to transfer funds directly from their Individual Retirement Account (IRA) to a qualified charitable organization, but you cannot make a QCD directly to a Donor-Advised Fund.

A QCD allows IRA owners to satisfy their required minimum distributions (RMDs) without incurring taxable income on the distributed amount.

The QCD is excluded from taxable income and counts toward the IRA owner’s annual RMD requirement.

This can be beneficial for those who do not need the funds for personal use and want to support charitable causes instead.

1. Limitations on QCDs

The IRS imposes certain limitations on QCDs. The maximum annual amount eligible for a QCD in 2025 is $108,000 per taxpayer.

This limit applies to the total QCDs made in a calendar year, regardless of the number of charities involved.

Learn more about the Benefits of Qualified Charitable Distributions in our comprehensive article! Explore how this strategic approach can help you support your favorite causes while potentially reducing your taxable income.

2. Eligible Recipient

The QCD must be made directly to a qualified charitable organization. A Donor-Advised Fund itself is not considered a qualified charitable organization for QCD purposes.

As with all giving strategies, it’s important to consult with a qualified tax advisor or financial professional to fully understand the specific rules and implications of QCDs and how they might fit into your overall giving strategy along with a DAF.

These advisors can provide guidance on how to navigate the process, ensure compliance with IRS regulations, and help optimize the tax benefits associated with charitable giving.

Next Steps

In conclusion, Donor-Advised Funds offer a convenient and impactful way to support charitable causes. They provide flexibility, immediate tax benefits, and opportunities for multigenerational giving.

But let’s face it, navigating the complex world of Donor-Advised Funds can feel overwhelming.

Don’t worry — at the Convoy of Hope Foundation, we’ve got you covered! We provide a simple, four-step process that makes sure your wealth is maximized for the greatest impact.

Step 1

Meet With

Our Team

They will work toward understanding your unique giving desires and how to pair those goals with the appropriate financial strategies.

Step 2

Create Custom Giving Road Map

Our team will create your custom giving road map — a detailed plan charting the course to your unique destination.

Step 3

Meet With Your Tax or Financial Advisor

Don’t worry, we’ll guide you through this process to ensure you’re confident in your ability to communicate what you want to accomplish.

Step 4

Ongoing

Check-Ins

Your financial plan is a marathon, not a sprint — we’ll provide ongoing check-ins to make sure you’re on track to reach your goals.

Schedule a call today and let’s kick off your journey to becoming a wise giver. Together, let’s make lasting positive change in this world.

*Disclaimer: Convoy of Hope and Convoy of Hope Foundation do not provide legal, tax, investment, or financial advice. The information in this article is intended for educational purposes only and should not be construed as professional advice. Donors are encouraged to consult with their own legal, tax, investment, or financial advisors when evaluating gifts to charity. Convoy of Hope and Convoy of Hope Foundation disclaim any liability arising from reliance on information provided herein.