A Smart Strategy for Lifelong Giving & Financial Stability

In a world where philanthropy meets financial planning, charitable gift annuities have emerged as a powerful and impactful way to support the causes you care about while securing a stable income stream for life.

In this comprehensive guide*, we’ll explore:

- • The ins and outs of charitable gift annuities.

- • How they work.

- • Their rates.

- • Potential benefits.

- • How you can use an Individual Retirement Account (IRA) to contribute to this charitable endeavor.

Let’s dive in!

What Is a Charitable Gift Annuity?

At its core, a charitable gift annuity is a unique arrangement that marries philanthropy with personal financial goals.

It involves making a charitable donation to an organization of your choice — often a nonprofit — in exchange for regular fixed payments for the rest of your life.

This arrangement serves a dual purpose:

- • It allows you to give back to your community.

- • Helps ensure financial stability during your retirement years.

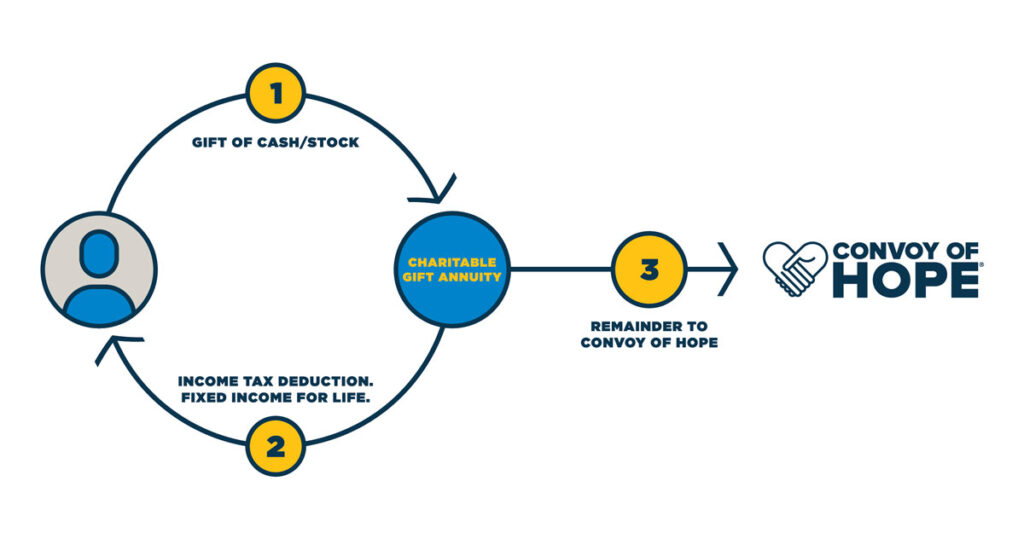

How Does a Charitable Gift Annuity Work?

Imagine you’re looking to contribute to a charitable cause while also securing your own financial future.

A charitable gift annuity allows you to achieve both objectives simultaneously.

Here’s a simple breakdown of the process:

Step 1. Making the Donation

You contribute a certain amount of money, securities, or even real estate to the chosen nonprofit organization.

Step 2. Fixed Payments

In return for your contribution, the charity promises to provide you with fixed payments for the rest of your life.

These payments are structured based on:

- • Your age.

- • The amount of your donation.

- • Prevailing charitable gift annuity rates.

Fixed payments received from a charitable gift annuity are typically subject to taxation, but not the entire payment amount.

The payments are divided into two components.

1. Taxable Portion

The taxable portion of the fixed payments is considered ordinary income and is subject to income tax.

This portion represents the difference between the total payment received and the “tax-free” portion.

2. Tax-Free Portion

The tax-free portion of the fixed payments is considered a return of the donor’s original contribution.

This portion is not subject to income tax.

7 Ways To Give Smarter

Learn how to create a giving strategy that aligns your resources, values, and goals to make a meaningful difference.

Topics include:

— Donor-advised funds

— Donating stocks

— Donating from your IRA

— Optimizing your business sale

Download Our Guide to Smarter Giving!

Start your journey toward using your income to make a difference, leave a legacy, and enrich lives.

":" indicates required fields

Calculating the Tax-Free Portion

The calculation of the tax-free portion depends on various factors, including the age or ages of the donors at the time the annuity was established.

Generally, the older the donor, the larger the tax-free portion.

This is because the charitable organization expects to make payments for a shorter duration for older donors, making a larger portion of the payment a return of the donor’s original contribution.

Charitable Income Tax Deduction

It’s important to note that donors may be eligible for an income tax deduction in the year they establish the charitable gift annuity.

This deduction is based on the present value of the charity’s future interest in the annuity.

The exact deduction amount varies depending on factors such as:

- • The donor’s age.

- • The contribution amount.

- • The prevailing discount rate set by the IRS.

Drawbacks of Charitable Gift Annuities

While charitable gift annuities offer a compelling blend of philanthropy and financial planning, it’s essential to be aware of their potential drawbacks.

Understanding the negatives can help donors make informed decisions about whether this option aligns with their goals and circumstances.

Here are some considerations to keep in mind.

1. Irrevocable Nature

Once a charitable gift annuity is established, it’s irrevocable.

This means that donors cannot change their minds or modify the terms of the arrangement once it’s in place.

2. Fixed Payments

While fixed payments ensure a lifetime income, they might not keep pace with inflation or changing economic conditions.

Over time, the purchasing power of these payments could diminish, impacting the donor’s ability to maintain their desired lifestyle. This is especially true during longer retirement periods.

3. Tax Implications

While there are tax benefits associated with charitable gift annuities, there are also other tax considerations.

Donors should consult with tax professionals to understand how the arrangement will impact their overall tax situation, including income tax, estate tax, and potential capital gains tax implications.

Can You Fund a Charitable Gift Annuity With an IRA?

For those who hold an Individual Retirement Account (IRA), there’s an exciting opportunity to channel your retirement funds into charitable gift annuities.

Through a qualified charitable distribution (QCD), you can directly transfer funds from your IRA to a charity, which then establishes a charitable gift annuity on your behalf. Note that the current maximum one-time contribution from your IRA is $54,000.

This approach has several advantages, including:

- • Reducing your taxable income.

- • Potentially lowering your required minimum distribution (RMD).

- • Supporting the charitable causes you hold dear.

Charitable Gift Annuity Rates & Payouts

The rates for charitable gift annuities are influenced by several factors, including your age and prevailing interest rates.

Generally, older individuals receive higher rates due to the shorter life expectancy calculation.

The American Council on Gift Annuities sets suggested maximum gift annuity rates, guiding organizations in offering competitive rates that benefit both the donor and the charity. These rates are reviewed periodically and are adjusted to ensure that they align with current economic conditions.

The October 21, 2024, suggested maximum rate schedules from the American Council of Gift Annuities are:

Single Life Suggested Maximum Gift Annuity Rates

Two Lives – Joint & Survivor Suggested Maximum Gift Annuity Rates

As a part of an ongoing monitoring process, the ACGA Board convened a meeting on October 21, 2024, during which it thoroughly examined the prevailing assumptions that underlie the suggested maximum rate schedules for gift annuities. For example, interest rates increasing has led to a decision to upwardly revise their suggested maximum payout rates.

Broadly speaking, the ACGA’s suggested maximum rates are meticulously crafted with a specific objective in mind — to culminate in a charitable gift amounting to 50% of the contributed funds for the annuity contract when the agreement reaches its culmination.

Are Charitable Gift Annuities a Good Idea?

Now, the big question — are charitable gift annuities a wise choice?

The answer depends on your unique circumstances and objectives.

If you’re passionate about giving back, seeking a reliable stream of income, and aiming to minimize potential tax burdens, then charitable gift annuities could be an ideal fit.

Not only do you make a difference in causes close to your heart, but you also benefit from a charitable income tax deduction, potential capital gains tax savings, and the satisfaction of leaving a legacy.

Next Steps

In the realm of philanthropy and financial planning, charitable gift annuities stand as a remarkable strategy. The concept of giving back while receiving fixed payments for life not only benefits you but also resonates with your desire to make the world a better place.

But let’s be honest. Navigating the complex world of charitable gift annuities can feel overwhelming.

Don’t worry — at the Convoy of Hope Foundation, we’ve got you covered! We provide a simple, four-step process that makes sure your wealth is maximized for the greatest impact.

Step 1

Meet With

Our Team

They will work toward understanding your unique giving desires and how to pair those goals with the appropriate financial strategies.

Step 2

Create Custom Giving Road Map

Our team will create your custom giving road map — a detailed plan charting the course to your unique destination.

Step 3

Meet With Your Tax or Financial Advisor

Don’t worry, we’ll guide you through this process to ensure you’re confident in your ability to communicate what you want to accomplish.

Step 4

Ongoing

Check-Ins

Your financial plan is a marathon, not a sprint — we’ll provide ongoing check-ins to make sure you’re on track to reach your goals.

Schedule a call today, and let’s kick off your journey to becoming a wise giver. Together, let’s make lasting positive change in this world.

*Disclaimer: Convoy of Hope and Convoy of Hope Foundation do not provide legal, tax, investment, or financial advice. The information in this article is intended for educational purposes only and should not be construed as professional advice. Donors are encouraged to consult with their own legal, tax, investment, or financial advisors when evaluating gifts to charity. Convoy of Hope and Convoy of Hope Foundation disclaim any liability arising from reliance on information provided herein.